Cluttons

GLOBAL GDP PERFORMANCE

Unsurprisingly, 15

12

political events 9

and public sector 6

spending are % 3

continuing to 0

greatly influence -3

-6

perceptions of 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Source: Markit /JP Morgan

domestic economic

*estimated from 2012 onwards

Singapore UAE* United Kingdom World

performance.

MARKIT JP MORGAN GLOBAL ALL-INDUSTRY OUTPUT PMI (2004 -2013)

60

Expansion

58

56

54

Output index value

52

50

48

Contraction

44

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

* Data for August 2013 Source: Markit /JP Morgan

Global PMI Output

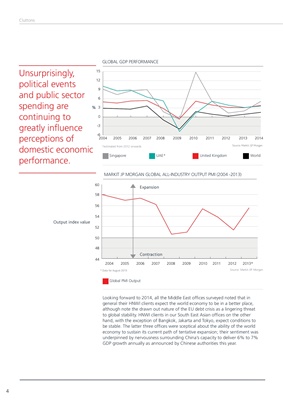

Looking forward to 2014, all the Middle East offices surveyed noted that in

general their HNWI clients expect the world economy to be in a better place,

although note the drawn out nature of the EU debt crisis as a lingering threat

to global stability. HNWI clients in our South East Asian offices on the other

hand, with the exception of Bangkok, Jakarta and Tokyo, expect conditions to

be stable. The latter three offices were sceptical about the ability of the world

economy to sustain its current path of tentative expansion; their sentiment was

underpinned by nervousness surrounding China’s capacity to deliver 6% to 7%

GDP growth annually as announced by Chinese authorities this year.

4