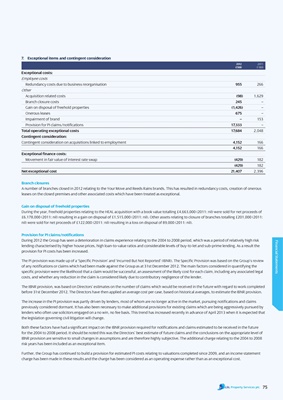

7. Exceptional items and contingent consideration

2012 2011

£’000 £’000

Exceptional costs:

Employee costs

Redundancy costs due to business reorganisation 955 266

Other

Acquisition related costs (98) 1,629

Branch closure costs 245 –

Gain on disposal of freehold properties (1,426) –

Onerous leases 675 –

Impairment of brand – 153

Provision for PI claims/notifications 17,333 –

total operating exceptional costs 17,684 2,048

contingent consideration:

Contingent consideration on acquisitions linked to employment 4,152 166

4,152 166

Exceptional finance costs:

Movement in fair value of interest rate swap (429) 182

(429) 182

net exceptional cost 21,407 2,396

Branch closures

A number of branches closed in 2012 relating to the Your Move and Reeds Rains brands. This has resulted in redundancy costs, creation of onerous

leases on the closed premises and other associated costs which have been treated as exceptional.

gain on disposal of freehold properties

During the year, freehold properties relating to the HEAL acquisition with a book value totalling £4,663,000 (2011: nil) were sold for net proceeds of

£6,178,000 (2011: nil) resulting in a gain on disposal of £1,515,000 (2011: nil). Other assets relating to closure of branches totalling £201,000 (2011:

nil) were sold for net proceeds of £122,000 (2011: nil) resulting in a loss on disposal of 89,000 (2011: nil).

Provision for Pi claims/notifications

During 2012 the Group has seen a deterioration in claims experience relating to the 2004 to 2008 period, which was a period of relatively high risk

Financial Statements

lending characterised by higher house prices, high loan-to-value ratios and considerable levels of buy-to-let and sub-prime lending. As a result the

provision for PI costs has been increased.

The PI provision was made up of a ‘Specific Provision’ and ‘Incurred But Not Reported’ (IBNR). The Specific Provision was based on the Group’s review

of any notifications or claims which had been made against the Group as at 31st December 2012. The main factors considered in quantifying the

specific provision were the likelihood that a claim would be successful, an assessment of the likely cost for each claim, including any associated legal

costs, and whether any reduction in the claim is considered likely due to contributory negligence of the lender.

The IBNR provision, was based on Directors’ estimates on the number of claims which would be received in the future with regard to work completed

before 31st December 2012. The Directors have then applied an average cost per case, based on historical averages, to estimate the IBNR provision.

The increase in the PI provision was partly driven by lenders, most of whom are no longer active in the market, pursuing notifications and claims

previously considered dormant. It has also been necessary to make additional provisions for existing claims which are being aggressively pursued by

lenders who often use solicitors engaged on a no win, no fee basis. This trend has increased recently in advance of April 2013 when it is expected that

the legislation governing civil litigation will change.

Both these factors have had a significant impact on the IBNR provision required for notifications and claims estimated to be received in the future

for the 2004 to 2008 period. It should be noted this was the Directors’ best estimate of future claims and the conclusions on the appropriate level of

IBNR provision are sensitive to small changes in assumptions and are therefore highly subjective. The additional charge relating to the 2004 to 2008

risk years has been included as an exceptional item.

Further, the Group has continued to build a provision for estimated PI costs relating to valuations completed since 2009, and an income statement

charge has been made in these results and the charge has been considered as an operating expense rather than as an exceptional cost.

75